Financial instability in the UEMOA: Niger faces record levels of unpaid loans

The January 2026 economic report reveals a concerning paradox within the West African Economic and Monetary Union (WAEMU): while the banking sector is reaching new heights in total credit, it is simultaneously battling a surge in financial risks. Niger, in particular, has emerged as the epicenter of this instability, recording a level of non-performing loans that highlights a widening economic gap across the region.

Niger: A critical peak in asset degradation

As the Union strives to maintain a stable financial framework, Niger’s indicators remain the most troubling in the zone. Despite a minor statistical improvement, the nation continues to be the most vulnerable component of the regional banking infrastructure.

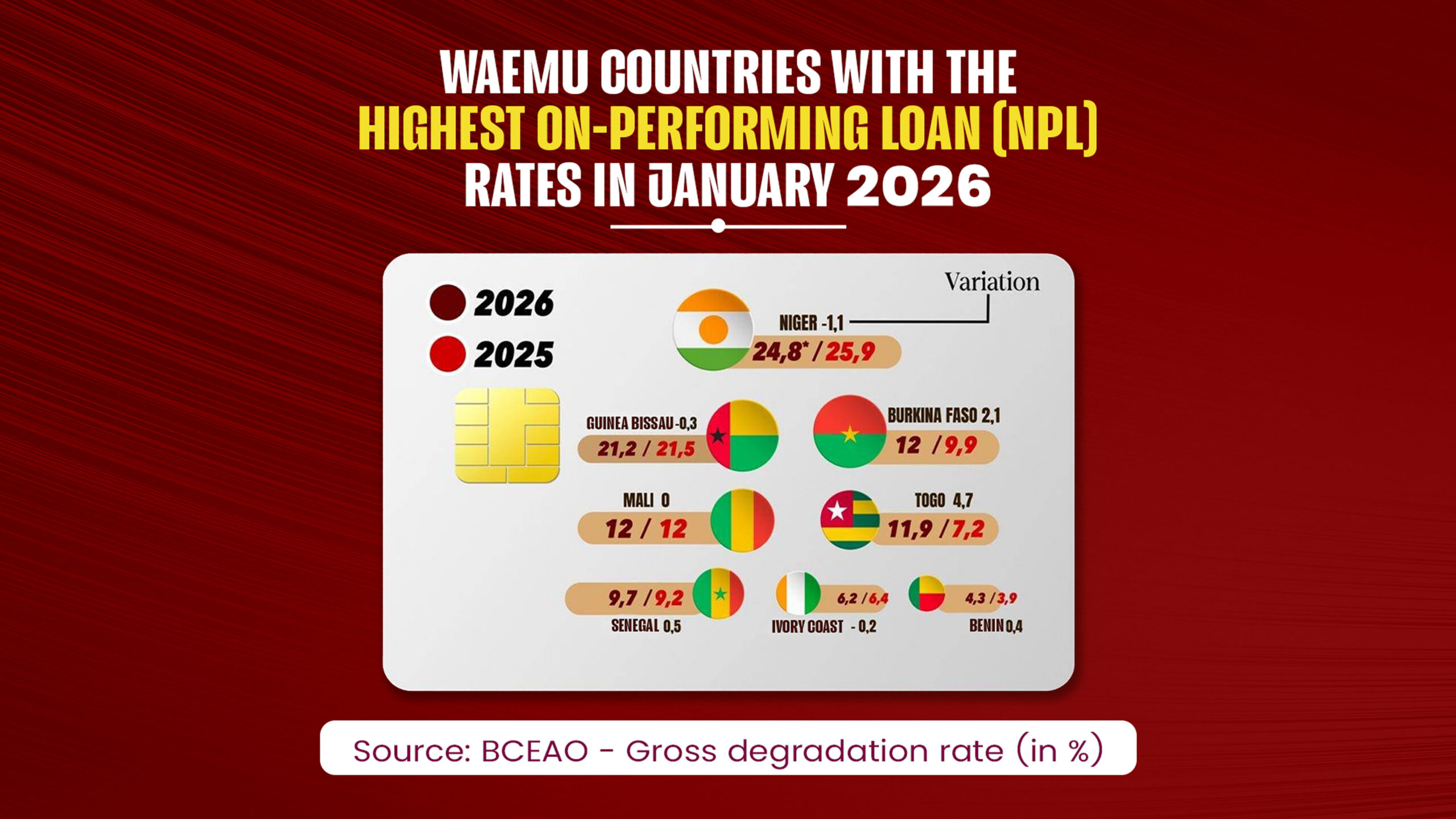

- A record-breaking default rate: With a gross degradation rate of 24.8% in January 2026, Niger holds the highest percentage of unpaid debts. This means nearly one out of every four credits issued in the country is currently in default.

- Structural fragility: Although this figure represents a slight decrease from the 25.9% recorded in 2025, the massive disparity compared to the regional average points to an extraordinary level of risk, largely driven by political instability and security challenges.

A fragmented union: The Sahelian vs. coastal divide

The data from early 2026 confirms a distinct separation between the coastal economies and the Sahelian bloc, where financial pressures are most acute.

1. Sahelian nations under pressure

Beyond Niger, other countries in the Sahel are seeing their financial health decline:

- Mali and Burkina Faso: Both nations have reached a 12% non-performing loan rate. Burkina Faso is of particular concern, having seen a sharp increase of 2.1 percentage points within a single year.

- Guinea-Bissau: This nation remains in a critical state with 21.2% of its loans classified as unpaid.

2. Relative stability in coastal regions

In contrast, coastal countries have generally managed to maintain higher quality loan portfolios, though some exceptions exist:

- Benin: Standing as the regional leader in stability, Benin boasts the lowest default rate at just 4.3%.

- Ivory Coast and Senegal: These economies show relative resilience, with rates of 6.2% and 9.7% respectively.

- The Togolese anomaly: Togo has deviated from the coastal trend, experiencing a significant surge in unpaid loans, which jumped from 7.2% to 11.9%—an increase of 4.7 points.

Global overview: Record credit levels met with banking caution

While the total volume of credit to the economy surpassed the historic milestone of 40,031 billion FCFA—marking a 4.7% annual increase—the momentum is being dampened by rising caution.

The warning signs: Total non-performing loans have reached 3,631 billion FCFA. Simultaneously, the coverage ratio has slipped to 59%, indicating that banks are struggling to provision for losses as quickly as new defaults are occurring.

Consequences of the slowdown

Due to the deteriorating risk profiles in nations like Niger, financial institutions have pivoted their strategies:

- Stricter lending criteria: Banks are now demanding higher personal contributions and more robust guarantees.

- Increased selectivity: Financial institutions are prioritizing balance sheet security over the expansion of credit, a move that could potentially restrict funding for local SMEs and SMIs.

As 2026 begins, the WAEMU banking system stands at a crossroads. While the overall structure remains intact, the situation in Niger and the potential for risk contagion across the Sahel demand constant oversight to prevent a regional liquidity crisis.